|

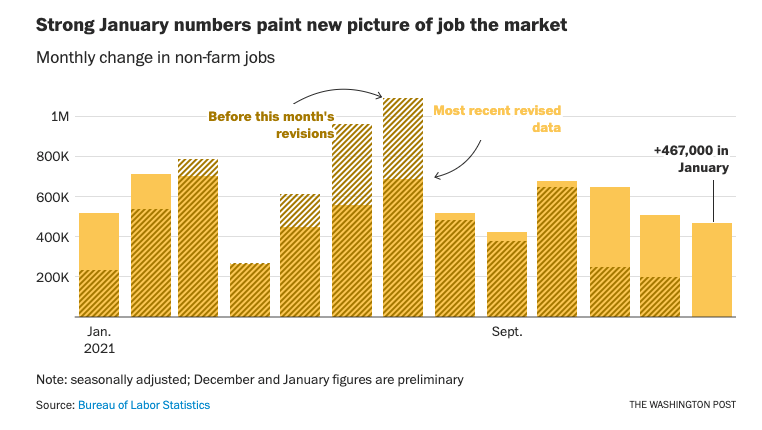

Last week, we reported here that there were deep concerns in some quarters regarding the strength of the economic recovery, with expert predictions of a slowing in growth and GDP. With the January report, as well as the corrections posted in the November and December reports, it remains to be seen if the recent projections of lower GDP and decreased job growth stand.

Labor force participation rate continues to climb

As reported by Reuters, "Employment could increase further as coronavirus infections continue to subside. First-time applications for unemployment benefits dropped for a second straight week last week.

But the labor force participation rate, or the proportion of working-age Americans who have a job or are looking for one, increased to 62.2% due to the changes in the composition of the population, from 61.9% in December.

The workforce increased by 1.393 million people. The employment-to-population ratio rose to 59.7% from 59.5% in December.

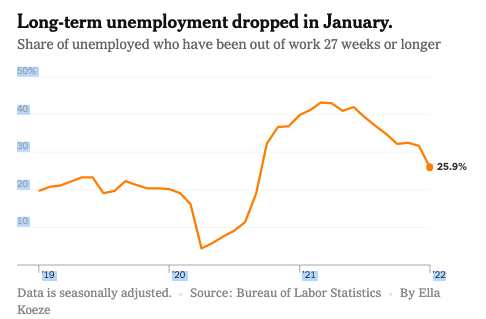

A broader measure of unemployment, which includes people who want to work but have given up searching and those working part-time because they cannot find full-time employment, dropped to 7.1%, the lowest since February 2020, from 7.3% in December".

Will the Fed Cool the Economy?

Consumer prices increased by 7 percent in December from the prior year, the fastest rise since 1982. Due to increased spending running up against persistent supply chain driven shortages, the hopes of inflation being temporary have been shown to be premature.

In response, the Fed, whose task it is to set economic policies to maintain full employment and stable prices, has slowed bond purchases faster than anticipated, and has signaled more interest rate increases.

As reported by the New York Times, "The Fed is on track to end its asset buying program in March, at which point markets expect policymakers to begin raising interest rates. Investors expect officials to raise interest rates as many as four times this year, while allowing their balance sheet of asset holdings to shrink. Both policy changes would work together to remove juice from the rapidly recovering economy".

We don't live in a bubble

No matter what the Fed does, it can't control the economic policies of other countries such as the U.K, the European Union or China. Depending on inflation, the pandemic, internal politics and a host of other factors, it will be difficult for the Fed to match its' actions with theirs.

U.S. Employers are betting on themselves

With caveats, it would appear that the U.S. economy is on firmer ground than thought just a month ago. Indications are that this will continue. U.S. employers are betting on themselves. It's been a long time coming, but the sun seems to breaking through.

|